Health Care Reform: Basic Health Plan and Bridge Plan Options

TO: HASC Board, March 27, 2013, Agenda Item II.F.

FROM: Jim Lott, Executive Vice President, Policy Development and Communications

SUBJECT: Health Care Reform: Basic Health Plan and Bridge Plan Options

RECOMMENDED ACTION:

Receive the report; advise staff.

BACKGROUND:

The Issue

Should California hospitals support a Basic Health Plan (BHP), as provided for by the ACA, to start up in 2015, and/or the creation of a “BHP-like” Bridge Plan to be operated by the state Exchange (Covered California) for low income populations to start up sooner, perhaps in 2014?

The Deal

ACA Structures and BHP Option

BHP and “BHP-like” proposals seek to address enrollment of the population between 139 percent and 200 percent of the Federal Poverty line (FPL). This translates to an annual income of $15,500 – $22,300 for an individual. These individuals do not qualify for coverage through Medicaid expansion via the ACA, but they are eligible to purchase health insurance coverage with federal subsidies through the state Exchanges.

While the individual health insurance mandate imposes tax penalties for failure to obtain coverage under the ACA, these penalties are often less than the out-of-pocket premium costs to the individual in this income range.(1) Furthermore, the collection of any penalties is dependent on submission of a tax return with a positive refund status.(2) In such an environment, individuals in the 139 percent to 200 percent of FPL range are less likely to obtain insurance under the individual mandate.(3) This adds to the population remaining uninsured under the ACA and places hospitals at financial risk should they eventually require care.

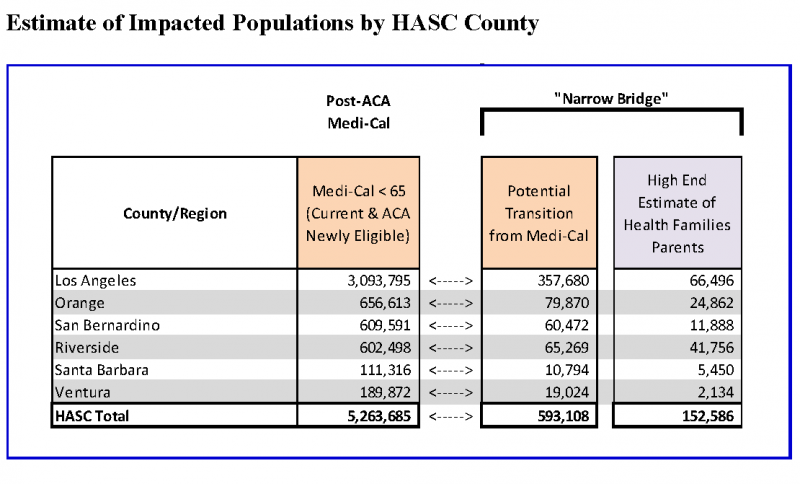

The ACA allows states to create a “Basic Health Plan” for uninsured individuals with annual incomes between 139 percent and 200 percent of FPL, as well as legally residing immigrants below 138 percent of FPL. For California, this represents about 930,000 individuals between 139 percent and 200 percent of FPL, and an additional 160,000 eligible legal immigrants.

If California were to offer a BHP, the target population would no longer be eligible for subsidies through the exchange. Rather, 95% of the monies that would have been paid by the federal government in subsidies for enrollees would go directly to the state for administration of the

BHP.

While a BHP is required to offer at minimum the same “essential health benefits” offered through the exchange, the BHP is free to define cost-sharing and delivery systems in such a way that would lower the overall out-of-pocket expense to this target population and encourage enrollment. This would likely be achieved through use of existing Medi-Cal Managed Care networks with similar provider rate levels.

Covered California “Bridge Option”

Covered California has recently proposed a “BHP-like” option within the framework of the exchange targeted at the population between 139 percent and 200 percent of FPL.

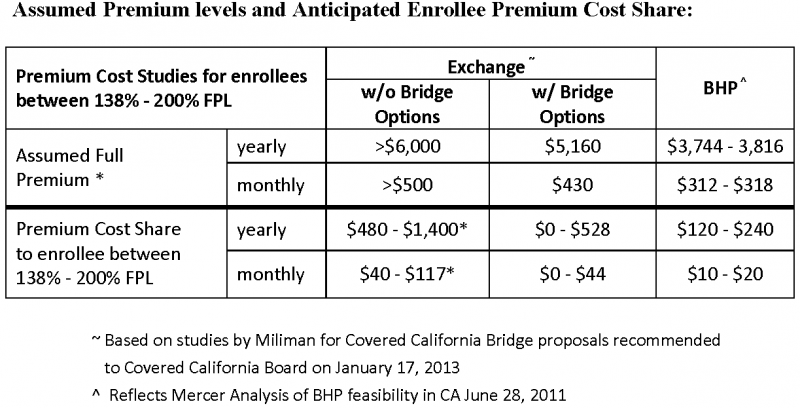

Rather than establish a separate BHP, Covered California proposes using the ACA subsidy structures to finance and create a “Bridge Plan” option within Covered California. The premiums for the Bridge Plan option would be targeted through the Exchange’s power of “selective contracting” to make the subsidized out-of-pocket premium cost to the target population low enough to encourage enrollment.

ACA premium subsidies to eligible individuals are based on the second lowest Silver Plan in the exchange and adjusted to the individuals’ income. As conceived, the Bridge Plan premium would be set at an amount approximating the lowest Silver Plan premium within the Exchange, resulting in a premium set at about 15% lower than the second lowest Silver Plan. To achieve this lower premium level, Covered California would negotiate contracts with existing Medi-Cal Managed Care plans to provide coverage for the target population.

Covered California’s Bridge Plan option provides a low-cost transition to individuals who start out on Medi-Cal, but due to fluctuations in income levels temporally lose eligibility status for a portion of the year (often associated with seasonal employment). In addition to income requirements, prior coverage under Medi-Cal within a window of time would be a prerequisite for coverage under this option. The plan targets the population that “churns” between being Medi-Cal and uninsured status, and it offers the ability to provide coverage through a single

payer and network. The churning population is estimated at 1.1 million individuals statewide.

This option will also be offered to parents of Health Family children with family incomes up to 250 percent of FPL so as to maintain unified coverage for the family with a single payer. Healthy Family parents are estimated to represent an additional 150,000 – 300,000 individuals.

To ensure the timely creation of networks to accommodate a Bridge Plan option within the exchange for 2014, Covered California will also streamline and simplify the process for Qualified Health Plan certification for Medi-Cal Managed Care Bridge Plans. It remains to be seen to what extent such relaxation of the process would permit use of existing Medi-Cal contracts with providers.

Key Issues

Both BHP and BHP-like options address the issue of affordability to potential enrollees between 139 percent and 200 percent FPL by offering a premium cost share level lower than would be experienced by individuals in this income range if they were obtaining their benefits in the exchange with federal subsidies, but without a bridge option.

It is generally agreed that a BHP or BHP-like program with more affordable premiums will result in greater enrollment for the targeted population. In modeling a potential BHP offering for California, the Urban Institute placed the marginal increase in coverage at 100,000 additional individuals under an ACA implementation with a BHP option than without.(4) A similar model run by UC Berkley/UCLA placed the marginal increase of enrollees in the range of 60,000-120,000. It should be noted that the upper range of the Berkley/UCLA study assumed the BHP plan network had a similar scope and reputation of a commercial plan, not that of a Medi-Cal plan.(5)

To achieve the target premium cost share levels for the envisioned Bridge Plan option, Covered California would, in essence, be manipulating the premium structure of the exchange in a manner that places downward pressure on provider rates. In addition to disregarding the true cost of delivering care to produce target premiums for the Bridge Plan option, the resulting premium supplants the “naturally” lowest Silver Plan option in the Exchange and bumps it up into the second lowest position. This displacement is significant because the federal government uses the second lowest Silver Plan to determine the level of subsidies in the exchange. A lower reference premium sub-optimizes the level of subsidies from the federal government (exchange subsidies are provided for enrollees up to 400 percent FPL).

Unlike a separate BHP, the Bridge Plan option brings the target population into the Exchange environment. However, the population would be concentrated in Medi-Cal Managed Care plans rather than spread across the array of Exchange private plans and their broader provider networks. Concerns regarding enrollee access to providers would exist.

Next Steps

Implementation of the Bridge Plan option within the Exchange will require federal approval and state legislative authorization. SBx3 (Hernandez) has been introduced in the 2013-14 Special Session to make this happen.

(1) An individual with an income of 138 percent of FPL could be responsible for up to $480 in yearly premium (3% of income) after subsidy in an exchange structure, but penalties for this individual would range from $155 in 2014 to $388 in 2016. (2) IRS is empowered only to seize tax refunds as payment toward unpaid penalties. (3) Currently in Medi-Cal, where the financial barriers to obtaining coverage through the state are limited, only 61.7% of the eligible population actually obtains coverage (UCLA/Cal Berkley, June 2012). (4) Urban Institute “Basic Health Plans: Issues for California” August, 2011 (5) UC Berkley/UCLA “Estimating the Change in Coverage in California with a Basic Health Program” August, 2012